Throughout the financial press, so-called experts are warning of the return of inflation. Should we be worried? Nobody likes rising prices for their everyday expenditures. But if the companies you’ve invested in are able to charge higher prices, shouldn’t that mean more profit and rising stock prices for your portfolio?

We are still in the longest bull market in history. We’ve had steadily rising stock prices for over 12 years without a sustained decline of over 20%. During that time, inflation has never risen above 3%. In fact, inflation hasn’t been above 3% since 1991 except for one important year – 2007(4.08%). The following year, the market saw its worst crash in history during the financial crisis of 2008.

What is it about lack of inflation that keeps a bull market going, while the return of inflation brings the bears out of hibernation?

What we learned during the first eighty years of the 20th century is that inflation causes unwanted instability. Let’s look at the extreme example of Brazil during the late 80’s and early 90’s, where they experienced monthly inflation as high as 100%. That means the price of a basket of goods was doubling every month… Or over 2000% per year! When that happens, people start to buy and hoard more goods because of the expectation that the price will double by the end of the following month. The extra buying drives up prices even more. Generally, wages are much slower to rise in response and we get a massive disconnect between what people earn and what basic necessities cost. There is no quick fix to a situation like this. To wit, Brazil was stuck in this cycle for over seven years. In North America, our last horrible bout with inflation was 1979/1980 when inflation hit 13%. What followed was the highest gold price we have seen in history and a stock market that was in decline for the next year and a half.

But it’s not the disease that causes markets to crash, it’s the cure. The only way to keep inflation under control is to take money out of the economy. With less money chasing the same number of goods, prices fall, inflation stays under control, and stability persists. There is only one practical tool available to take money out of the economy – increase interest rates. When interest rates rise, fewer people/governments/companies can afford to borrow. Less borrowing = Less money in the economy.

Think of it this way – You buy a house for $1 Million and you borrow $800,000 through a mortgage. The person you bought the house from takes the $1 Million and deposits it in the bank… which in turn allows the bank to lend out another $800,000 to someone else. All of a sudden one loan of $800,000 has turned into two. And we now have double the amount of money injected into the economy. But if we raise interest rates, this won’t happen as easily. In fact, many people and businesses will pay off debt as interest rates rise, further accelerating the reduction of money in the economy. When you add the people/businesses that go bankrupt because of the higher cost of debt, to the shrinking amount of money due to those paying off their debt, you’ve got a whole lot less money being spent. The economy starts to shrink. People lose their jobs. The cycle gets worse. Company profit starts to disappear and their stock prices collapse.

Every single bear market (with the possible exception of the dot-com bubble of 2000) has been kicked off by a rising interest rate environment. So “why raise interest rates?!”, you might ask. As central banks around the world have gotten better at keeping inflation at modest level by tweaking interest rates on occasion, our periods of sustained economic growth have gotten longer. It’s true that we still get stock market corrections and economic contractions when the perfect balance can’t be maintained. But common wisdom says that the payoff is a more steady, stable, growing economy for longer periods of time.

When the headline says “Beware Inflation”, it’s really saying “Wake up the bear, it’s time to raise interest rates”.

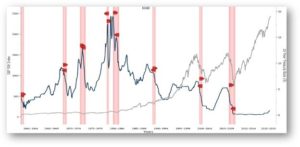

Rising interest rates and the effect on the markets

The pink columns represent significant market corrections. In almost all cases these corrections are preceded by a period of rising interest rates.

Thanks for reading!

We hope you enjoyed Issue #1 of “Wealth Matters for Dental Professionals”. We plan to keep bringing you interesting information and helpful insights into wealth management and investing over the coming weeks and months.